Value is in the eyes of the beholder. Obvious, but no less true for that. Of course, you might know a wealthy Saudi Arabian Oil Sheikh (or just a neighbour) who already wants to invest in your business – but, barring this eventuality, we are talking about utilising financial adviser marketing services to maximise the objective chances of meeting a higher valuation when the marketing/networking moment arises.

Professional advisers (Solicitors, Corporate Finance Accountants) – and lenders – will also rely on accepted metrics/objective assessments to validate the value that’s being discussed.

So, how do we use financial adviser marketing services to make ourselves look as good as possible?

Getting the Metrics Right

Maximising embedded value is about:

- Reducing (or certainly controlling) costs

- Maximising revenue

- Reducing risks

These steps are more likely to lead to ‘sustainable’ profit which acquirers will pay more for – on the basic “P/E multiple” principle. Which says, of course, that the price an acquirer pays will be a multiple of the average annualised earnings they anticipate. Mathematically, (and simply) this “p/e” ratio will give the number of ‘years’ it will take for the deal to pay for itself.

Some acquirers (like those who buy Premier League football clubs) may buy for kudos, or other emotive reasons – but for most people acquiring a business, it’s the return that is important. So the price someone is willing to pay for a business is linked to the belief in the return that the acquirer is likely to get over the journey of the investment.

When someone is conducting their review or ‘due diligence’ into a vendor’s business, they will look for both the ‘detractors’ and ‘enhancers’ to the valuation. These will conveniently spin-off from the same tripod of Cost, Revenue and Risk that we just examined.

What are the Enhancers to a Valuation?

Positive Value Enhancers – for an Advisory Business

(Valuation / Due Diligence / Industry Comparables)

- Properly segmented & communicated client propositions

- A consistent client experience – methods and process

- A de-risking of the advisory cycle. Client awareness and an audit trial

- Assets under management & influence

- Relevant and accurate client information

- Reliable business management information

- Predictability and expectation of business streams

- Brand articulation – buy clients – what they know & also value

- High persistency rates/low latent & actual) complaints (de-risking)

- Clear succession planning/staff progression

- Access to industry expertise/change assistance

- Scalability/potential to grow/’fleet of foot’ qualities

What Are the Detractors?

- Owner seeking immediate exit – owner/key client relationship holders leave businesses before appropriate succession planning/ implementation.

- Reliance on the owner for key clients – may lead to a greater proportion of consideration being deferred

- Reliance on a small number of clients – a high proportion of overall revenue is generated from a few clients results in lower multiple or discount applied to future revenues

- Poor quality of client records – can’t evidence how valuable clients are, management information is key

- Poor compliance monitoring – poor compliance monitoring will rule out most buyers, buyers apply a discount and allow for likely correction costs

- Current economic factors – current market multiplies reflect lower AUM’s, lower forecast revenues, lower propensity to invest, heightened cost and lack of debt.

- Anything that burgeons cost and risk – and limits revenue.

How Do We Market Ourselves For a Sale?

So, how can financial adviser marketing services help us best market ourselves? Good question. Acquirers will value based on the likelihood of a return – but, as with a house purchase, acquirers will be more likely to ‘take notice’ of the positive traits of a business if they are well packaged and well presented.

So – Management Information (MI) which is the right blend of concise summary and supporting info is essential as part of financial adviser marketing services. A ‘Vendor’s pack’ if you will, much in the way you would put your house on the market.

How Do We Make Ourselves Stand Out?

We live in an intangible financial services industry – however, if you can tell the personal story – and include what makes your business different as a part of your financial adviser marketing services, this will inevitably attract more attention. Testimonials or citations from clients will also help credibility, as will a strong articulation of your brand.

What Sort of Deals Can be Done?

Some deals are done to buy “the client bank” – or the assets of the business – and in old language, this was commonly done on “X times renewal”. Say, 2 to 3 times renewal. Remember, no one “owns” clients! – only the right/opportunity to market said clients. So this is about how loyal/attached the clients are to the vendor’s business and, how likely this is to transfer forward with the transition to the new acquirer. Since the language of RDR came in (meaning ‘adviser charging’), we widen ‘renewal’ to cover predictable, repeatable annual revenue which can be expected to come in each year.

(As long as any acquirer would expect to collect the same fees when they roll forwards the transaction – these could be included – such as with the old concept of “renewal”).

Other Deals?

Other deals are done on a figure of “X times EBITDA” – (Earnings Before Interest, Tax Depreciation & Amortisation) – or the annualised earnings. This seeks to find an annual figure for the ‘cash generation’ within the business – the purpose of EBITDA is to find a figure that can be more easily (fairly) compared and takes out any unusual/variable spending so the raw cash generation is shown. A figure of 5-7 x EBITDA is common in the financial advice industry.

How Is the Deal Completed?

What about the actual mechanics (method) of payment / in completing the deal? This is a very common issue when talking about financial adviser marketing services and sales. It is all about the negotiation. Although often, if a vendor seeks a large (or even entire) payment of the deal being ‘upfront’ or immediate, then all the risk sits with the acquirer and the acquirer will discount their offer, based on this risk.

Fast Versus Slow

In other words, a vendor might find it achieves a lower lump sum price if its wish is to walk off to their early exit (from the business) in a matter of days or weeks. The other, more gradual route moves through a spectrum of ‘remaining on board’ – through a form of ‘earn out’ period. And whilst an upfront % (of some 10 – 50%) is possible, the balance would then be earned over a 1-5 year period, post deal. This moves the risk further toward the vendor, who would essentially have ‘targets’ to meet, in order to achieve the fullest valuation pot figure.

Business Plan

The way the deals here are normally done is that a “business plan” is completed through the dialogue between the vendor and the purchaser – and the business plan will show a certain predicted ‘performance’ over the earn-out period. If the business plan is ‘met’ this would (for example) bring in “£X” amount of profit over the journey. If this is then divided by the (say) 3-year journey, we get the annual profit figure – and this can be given the “X times EBITDA” treatment.

This comes up with a ‘pot’ of deal money which is planned/anticipated. If this pot was, say, £1 million, then the parties might agree a 20% initial up-front payment (£200,000) with the balance of £800,000 only being earned if the business plan comes to fruition. The above is unlikely to be an ‘all or nothing’ balancing payment – but there would be a proportionate lessening of the balancing payment where the business plan was proportionately unfulfilled.

How Can I Get My Business Ship Shape?

The first step in financial adviser marketing services is recognising the need for change, and this is actually harder than people think.

Change in our industry is about our heart and our head.

When change happens, be it moving house or the retail purchase of a shiny iPod, M.R.I. scanning of our brain shows that it is emotion that drives our inclination to accept (or reject) the change presented before us. Not logic – but emotion. We are all humans, after all.

The following is a helpful ideogram that we use with Financial Advisory businesses: A.D.K.A.R

- Awareness of the need for change

- Desire to participate and support change

- Knowledge of how to change

- Ability to implement required skills and behaviours

- Reinforcement to sustain the change

An important lesson is to ensure inclusion & engagement (early on) from staff with allocated responsibilities for their own aspects of the ‘ship-shape’ change. People naturally prefer their own change contributions, over those directed to them, from on high.

So, to the practicalities

What steps can be taken with financial adviser marketing services that are going to help the business enhance its readiness?

We begin with a list of the proven “Value Enhancers” we saw earlier – the factors that due-diligence professionals use whenever they value the monetary worth of IFA Firms in our RDR context. And which will, in turn, define what they are willing to pay for this IFA – based also, of course, on industry comparables. A due-diligence professional will apply a collective of these criteria and will use a set of spreadsheets to apply scorings and “Monetary equivalence” calculations based on them.

They will further discount the valuation figures where they perceive uncertainty and risk (sitting either within the client bank or across the wider Firm’s governance). A due-diligence professional will not be swayed by emotional persuasions or standalone statements of belief – but will ask for evidence! and data that supports the case.

How can I address these points, then?

“By making a start” would be a common reply – and by receiving help and expertise.

For instance:

- By applying the FSA’s strong Risk Profiling guidance to demonstrate a clear coverage of “Tolerance, Capacity and Goals” in client risk profiling.

- By using the IFA’s own data and testing the “flexing” of customer propositions in order to show how loyal the IFA business is to the different segments declared. Is there discrete daylight between propositions, or do they morph into one another?

- By testing the different remuneration models against a mapping of client case sizes and client need scenarios – to examine the satisfaction of TCF as well as expected profit margins for the IFA business.

The Regulatory Side of Things

Elements of regulatory uncertainty remain; and whilst changes to the urgency & nature of any change is supremely relevant, a business implementing consistent, clean & de-risked processes (even outside of RDR) is a savvy one, for succession & competitive advantage.

Richard Komarniski (“The Human Factors”) comments on distraction and a lack of focus being the most common blockages to change – and whilst consultants will provide different quantities and qualities of guidance, the honest truth is that IFAs have much of the required ability & some (carefully apportioned) capacity to implement RDR change.

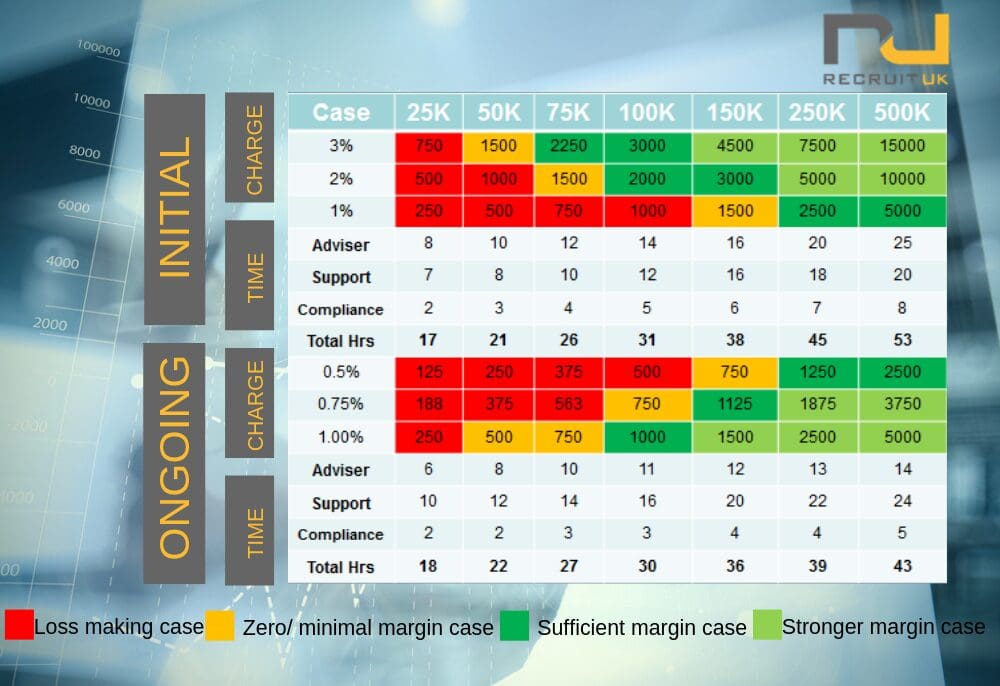

Mapping Advisory Time & Profitability

The following chart represents an IFA’s test of the average time spend (in hours) for different client case sizes. On simple mathematics, different remuneration charging leads to different profit margins (or losses). The empowerment this exercise offers the financial adviser is to add their own “hourly rate worth” and unique hourly spend data into their own calculations, to work out profit and loss.

The next step is to map a full spectrum of “Fit for purpose” Investment Solutions (from Full DFM, through Model Portfolios, OEICs, Index/Passive Funds/using an online Web/Portal) to ensure the IFA can offer robust advice, within a profitable framework.

- According to David A. Ricks “Blunders in International Business” – by far the most common reason for business goals failing is a lack of change.…not too much change!

- Aim high – a changing business should result with empowered, able staff with the skills to leave but the desire to stay.

- Processes that are robust & scalable – but hard for other businesses to copy from the outside.